When it comes to new bitcoin ETF money, BlackRock’s IBIT and Fidelity’s FBTC are capturing the overwhelming majority of inflows, while smaller issuers are increasingly pushed to the margins as institutional capital concentrates in the largest and most established funds.

When U.S. spot bitcoin ETFs launched in January 2024, investors had a broad lineup of more than a dozen products from firms including BlackRock, Fidelity, Ark Invest, Bitwise, VanEck, and Franklin Templeton, setting the stage for what was expected to be a highly competitive market.

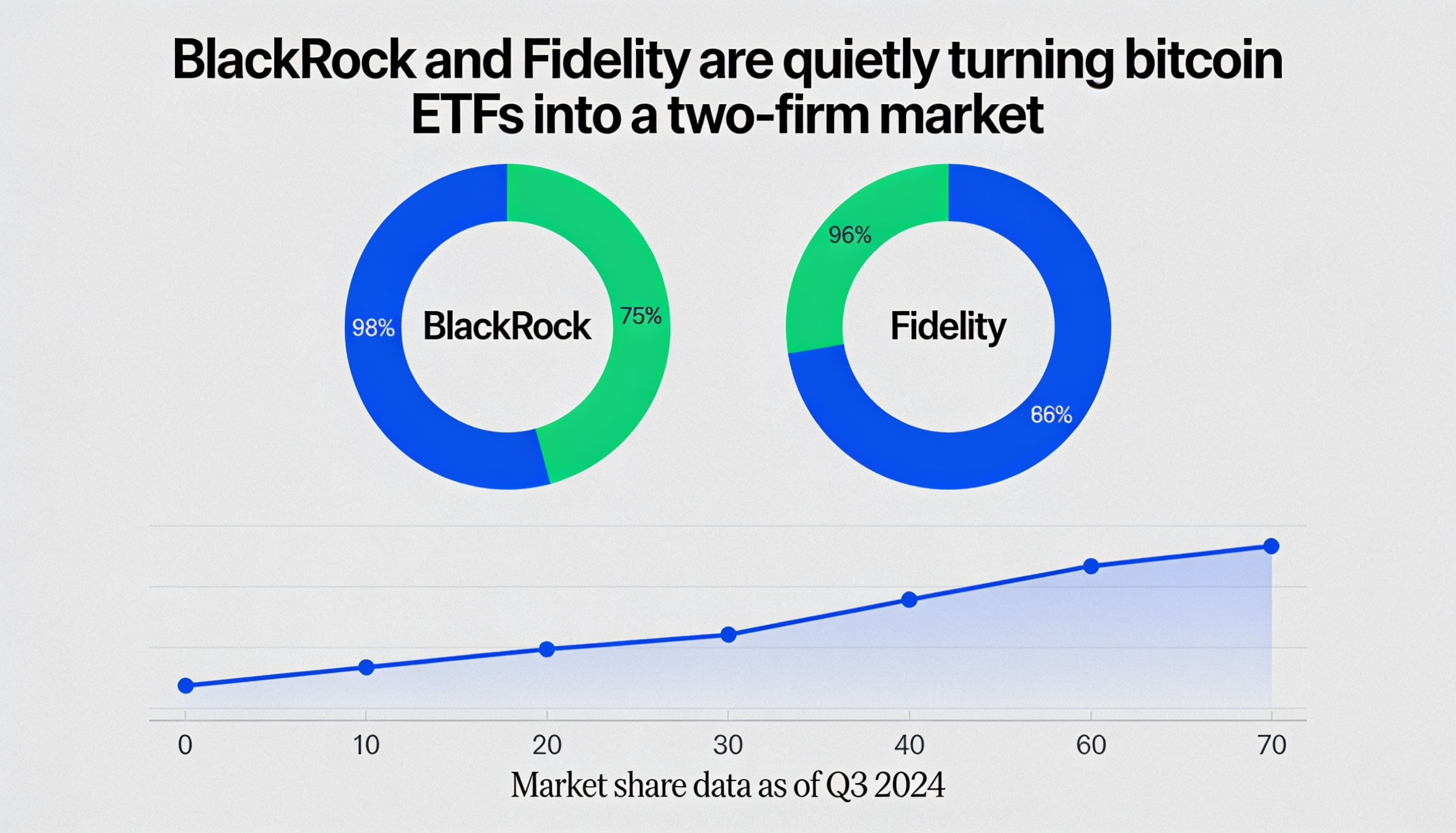

Eighteen months later, however, the landscape has effectively narrowed into a two-horse race.

Flow data shows that BlackRock’s iShares Bitcoin Trust (IBIT) and Fidelity’s Wise Origin Bitcoin Fund (FBTC) dominate most inflow days, while smaller ETFs have become far less influential in shaping overall market direction.

This pattern has been consistent through 2026.

For example, on January 14, bitcoin ETFs saw $840.6 million in net inflows, with IBIT alone contributing $648.4 million and FBTC adding $125.4 million—together accounting for more than 90% of the total. A similar dynamic played out on April 17, when IBIT and FBTC together made up roughly two-thirds of $663.9 million in inflows.

Even during softer market periods, the concentration remained clear. On May 1, total inflows of $629.8 million included nearly $500 million combined from IBIT and FBTC.

While year-to-date figures show some variation—such as stronger inflows into Grayscale’s Bitcoin Mini Trust compared with IBIT—overall allocation trends still show that BlackRock and Fidelity consistently capture the bulk of new capital whenever investors add exposure to spot bitcoin ETFs.

This concentration has developed during a challenging year for crypto markets, with bitcoin down roughly 29% year-to-date and ETF flows swinging between inflows and sharp redemptions. Periods of heavy selling in mid-May and early June marked a clear shift from earlier optimism, when dips were often viewed as buying opportunities.

Even so, capital flows increasingly favor scale and liquidity, reinforcing the dominance of the largest ETF providers.

BlackRock has been the biggest beneficiary of this shift.

IBIT has effectively become the flagship product of the entire sector, frequently leading inflows and often proving more resilient during market stress. On several days of broad ETF outflows, it either stayed positive or saw smaller redemptions than rivals.

That dominance is partly explained by the profile of buyers. Institutional allocators such as financial advisers, hedge funds, family offices, and pension consultants prioritize liquidity, brand trust, and execution quality as much as exposure itself.

With over $10 trillion in assets under management and deep distribution across global advisory networks, BlackRock brings unmatched reach. Fidelity similarly benefits from its established presence in both retail and institutional investing.

As a result, IBIT and FBTC have increasingly become the default entry points for bitcoin exposure.

At the same time, smaller ETFs are struggling to maintain relevance.

Funds from issuers such as Franklin Templeton, VanEck, Valkyrie, and WisdomTree often register only modest daily flows, frequently too small to meaningfully influence aggregate market trends.

Even previously competitive products from Bitwise and Ark now play a secondary role relative to the two leaders. Some entrants have already stepped back entirely, underscoring how difficult the market has become for new players.

During volatile periods, the pattern becomes even more pronounced: inflows and outflows are largely dictated by activity in IBIT and FBTC, effectively determining whether the entire ETF sector ends a day in positive or negative territory.

Taken together, the data suggests the bitcoin ETF market is evolving from a crowded field of issuers into a winner-take-most structure, where scale, liquidity, and distribution increasingly define success.