Bitcoin is edging toward a fifth straight weekly decline, and a clean break below current support could trigger another leg down.

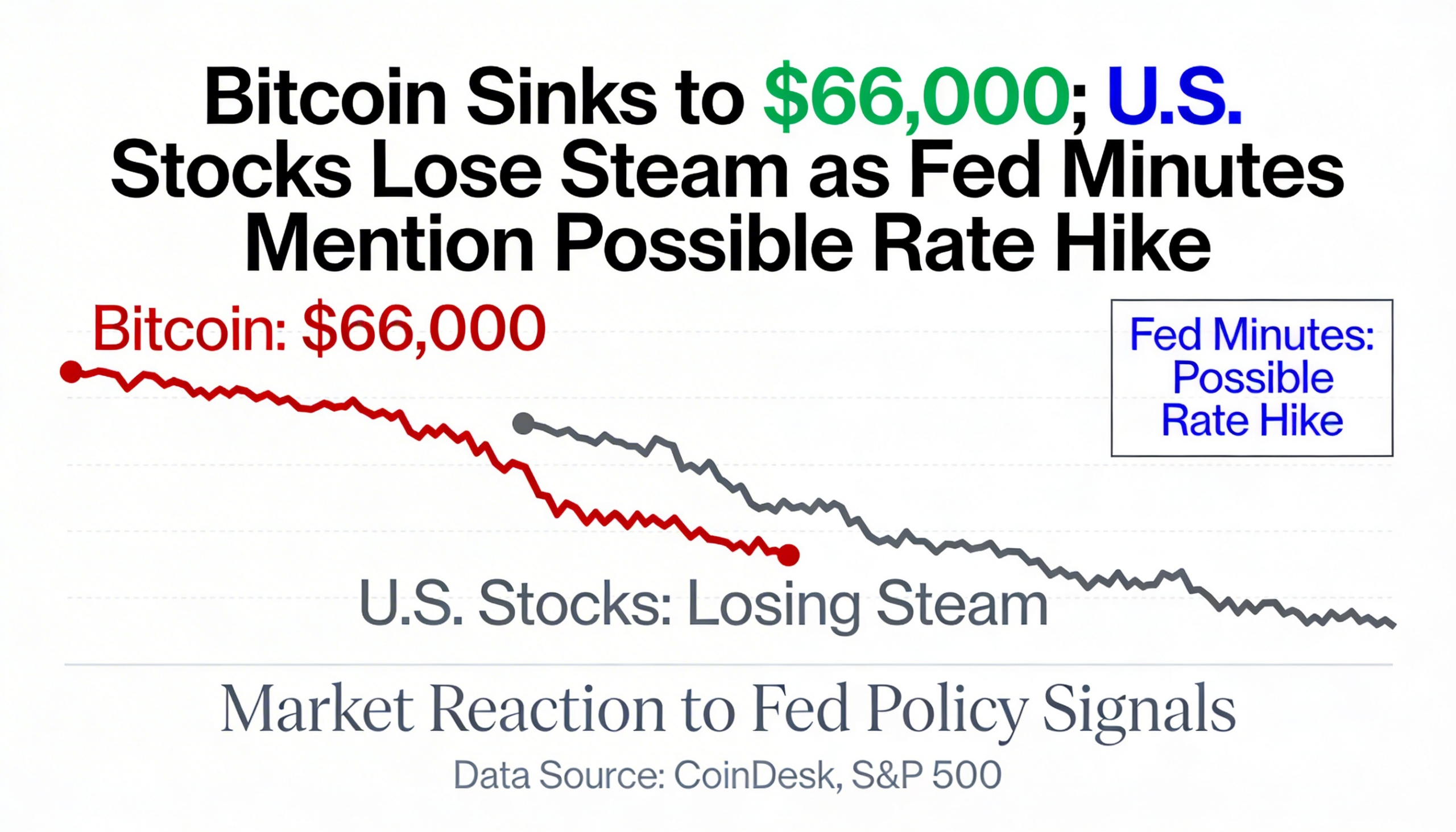

Price action was choppy early Wednesday before BTC turned lower during U.S. trading hours, sliding under $66,000 and retesting the bottom of its recent range. After changing hands around $68,500 overnight, the cryptocurrency fell roughly 2.5% over the past 24 hours to trade near $66,200.

Crypto-related equities mirrored the move. Coinbase erased an early 3% gain and slipped into a roughly 2% loss by the afternoon. MicroStrategy (MSTR), the largest public corporate holder of bitcoin, dropped about 3% as weakness in the underlying asset weighed on sentiment.

U.S. stocks also surrendered early advances ahead of the close. Contributing to the shift were minutes from the January meeting of the Federal Open Market Committee, which carried a more hawkish tone than expected. While officials broadly agreed on pausing rate cuts, several participants signaled support for “two-sided” guidance, suggesting the Fed could consider raising rates again if inflation proves persistent.

The U.S. dollar strengthened further in response. The U.S. Dollar Index climbed to a near two-week high, adding pressure to risk assets. A firmer dollar typically acts as a headwind for cryptocurrencies, and Wednesday’s pullback aligned with that pattern.

With the latest slide, bitcoin is now facing its longest weekly losing streak since the 2022 downturn. The $66,000 level remains a crucial support zone after holding last week and fueling a rebound above $70,000. A decisive breakdown below that threshold could shift attention toward early February lows near $60,000 — and potentially open the door to a deeper correction.