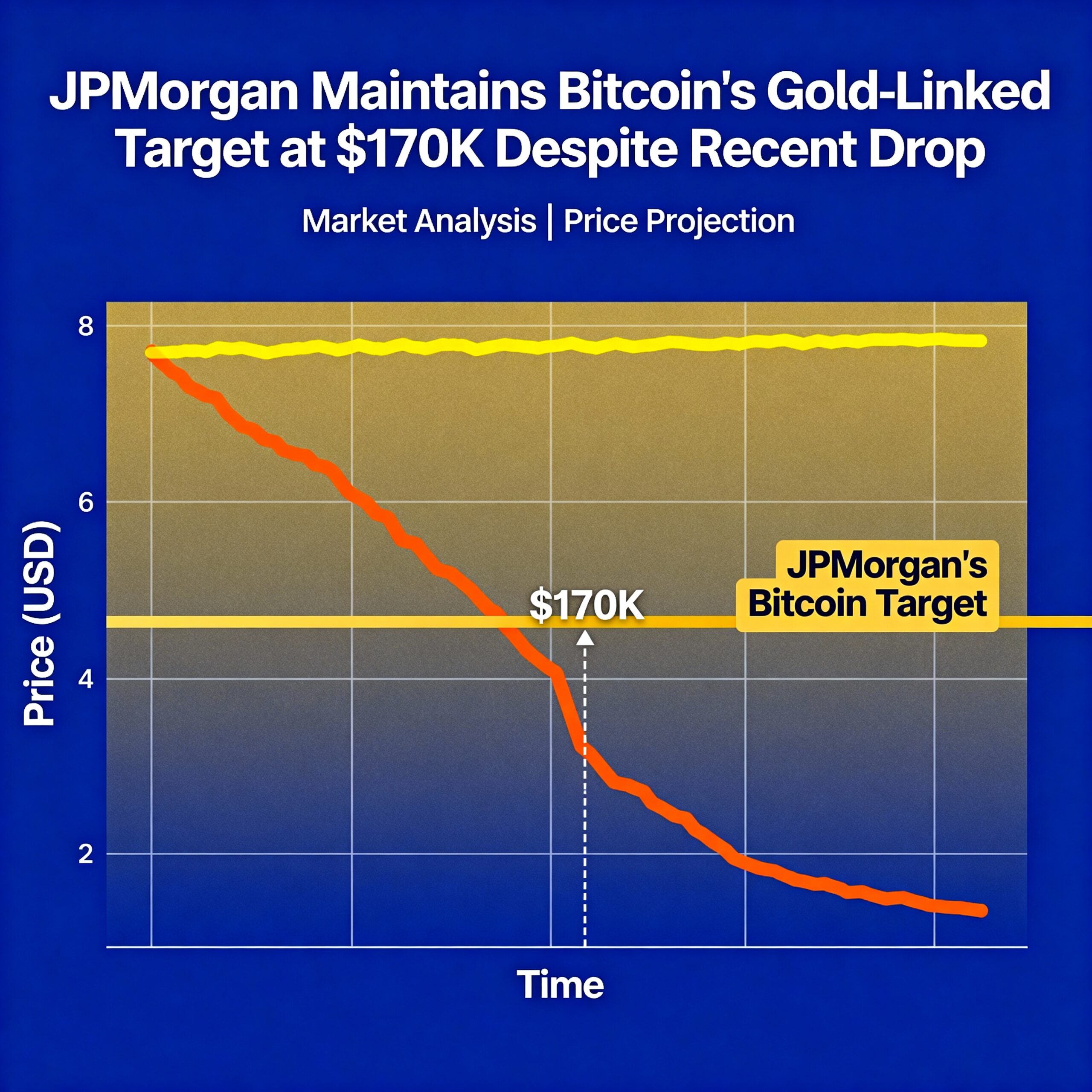

Despite recent sharp declines in Bitcoin’s price, JPMorgan continues to maintain its volatility-adjusted BTC-to-gold model, targeting a theoretical price of around $170,000 over the next six to twelve months.

Bitcoin was trading near $91,200 at the time of publication.

MicroStrategy (MSTR) remains a key market driver, with analysts closely monitoring its enterprise-value-to-bitcoin-holdings ratio (mNAV), currently around 1.13. JPMorgan analysts led by Nikolaos Panigirtzoglou noted that mNAV serves as a critical indicator of forced-selling risk if it falls below 1.0, though MicroStrategy’s mNAV remains safely above that level.

The company’s $1.4 billion cash reserve provides a buffer against the need to liquidate Bitcoin holdings. Analysts also highlighted the upcoming MSCI index decision on January 15 as a potential asymmetric catalyst: while exclusion is largely priced in after a significant share decline since October 10, a positive outcome could trigger a substantial rebound.

Founded by Michael Saylor, MicroStrategy is the largest corporate holder of Bitcoin, with 650,000 BTC on its balance sheet. The company has been under scrutiny as Bitcoin fell from an all-time high above $120,000 to around $82,000.

JPMorgan attributed part of the recent decline to renewed mining pressures in China and high-cost miners exiting elsewhere, some reportedly selling Bitcoin amid elevated energy costs. Following drops in network hash rate and mining difficulty, the bank lowered its estimate of Bitcoin’s production cost from $94,000 to $90,000.

A declining hash rate, which reflects total network mining power, can create a self-reinforcing cycle: marginal miners exit, difficulty decreases, and production costs fall—an effect observed during the 2018 market downturn, analysts noted.