While some market participants believe Bitcoin is being sold to raise liquidity ahead of major IPOs such as SpaceX and Anthropic, Sygnum CIO Fabian Dori argues that broader market data does not support that narrative.

Bitcoin exchange-traded funds (ETFs) have recorded nearly $5.75 billion in outflows since mid-May, intensifying speculation that institutional investors are reducing crypto exposure in anticipation of high-profile equity listings, starting with SpaceX’s expected debut.

The selling pressure contributed to Bitcoin sliding below $60,000 in early June, marking its weakest level since 2026 and a decline of more than 50% from its all-time high near $125,000 set last October. One widely discussed explanation has been a capital rotation out of crypto and into upcoming IPO allocations.

However, Fabian Dori of Sygnum is skeptical of this view.

“The ETF outflows are real,” he said in an interview with CoinDesk, “but the data does not truly support the idea that Bitcoin is weakening because of the SpaceX IPO.”

He noted that if investors were systematically liquidating Bitcoin to fund IPO participation, it would likely show up as abnormal exchange outflows and a clear drop in stablecoin market capitalization. According to him, neither trend is visible in current data.

Exchange activity remains broadly in line with historical norms, while stablecoin supply has not seen meaningful contraction. At the same time, riskier segments of the crypto market continue to attract inflows—behavior that would be inconsistent with investors exiting the asset class entirely.

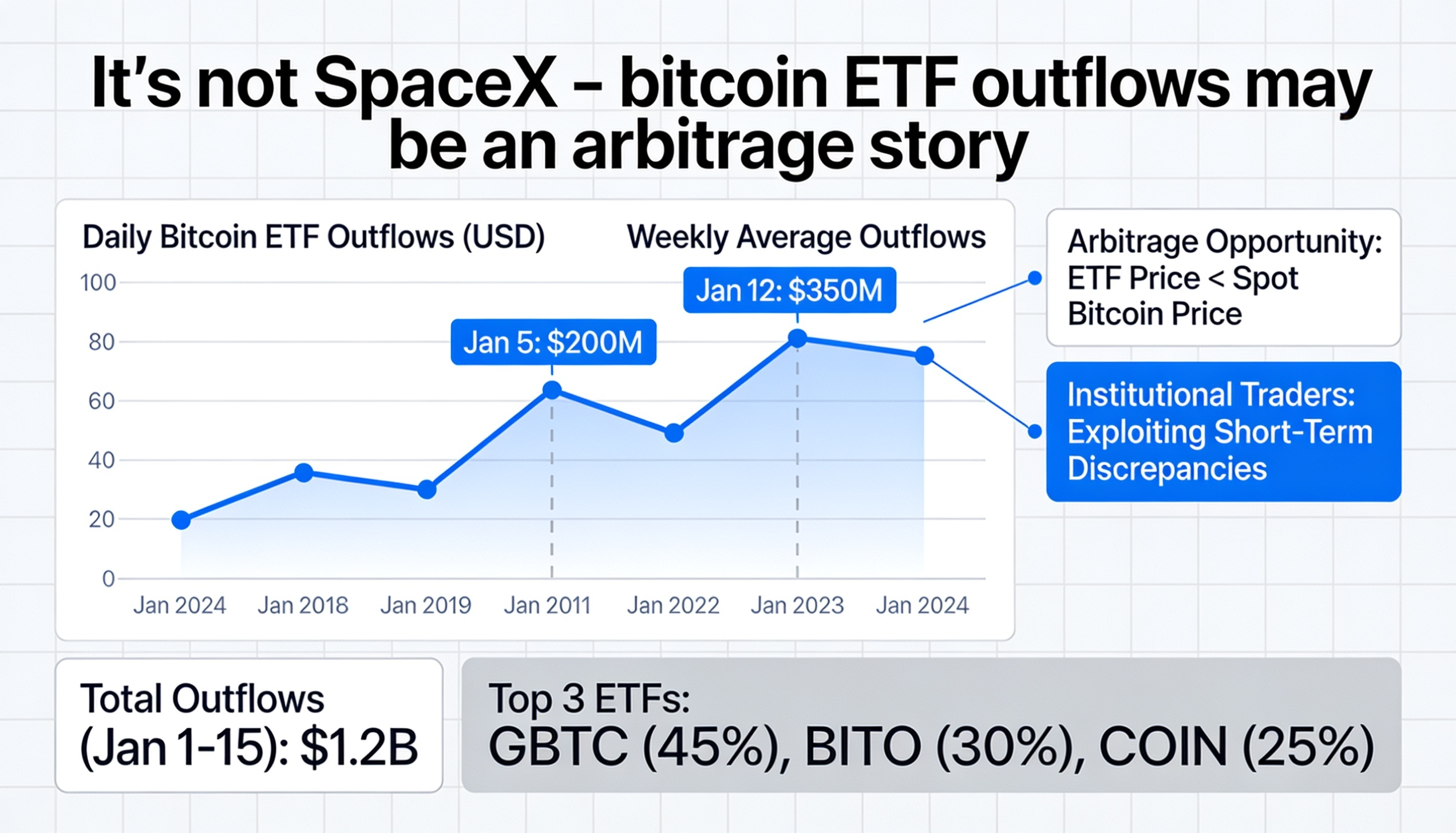

Dori argues that derivatives data offers an even clearer counterpoint to the IPO-rotation thesis.

He pointed to a decline in CME Bitcoin futures open interest occurring alongside ETF redemptions, suggesting that a large portion of the outflows may be driven instead by the unwinding of cash-and-carry arbitrage trades rather than capital shifting into equities.

Cash-and-carry arbitrage is a common institutional strategy that exploits the spread between Bitcoin’s spot price and futures contracts. Investors typically buy spot Bitcoin—often via ETFs—while simultaneously shorting futures. When futures trade at a premium, the spread generates a relatively low-risk return as prices converge at expiration.

When that spread compresses or funding conditions weaken, the trade becomes less attractive, prompting investors to close positions by selling spot holdings and covering futures shorts. This can produce ETF outflows even without a bearish shift in sentiment, as it reflects arbitrage unwinding rather than directional selling.

“Open interest and funding rates moved very positively together over the same period,” Dori said, adding that this alignment suggests ETF flows are largely tied to the unwinding of funding-rate carry trades rather than a broader exit from Bitcoin exposure.